English

EnglishHow to Drive Procurement Benefits from Spend Analysis

One of the most frequent questions we get from our clients is hands down: What is the best approach to use and identify savings opportunities through spend analysis?

This is an excellent question. There are a wide variety of opportunity analyses that can be conducted directly within a good spend analysis tool.

We find many of our customers and partners following a similar path time and time again with an overarching theme of “start with the basics and generate quick wins”.

1. Identify Leverage With Existing Suppliers

As part of our spend program we commonly include supplier linkage data (parent/child) which identifies corporate families.

This is as basic as it gets – gaining an understanding of which suppliers are owned by the same parent entity. In many cases existing agreements can be consolidated and renegotiated with the parent entity.

2. Supplier Rationalization

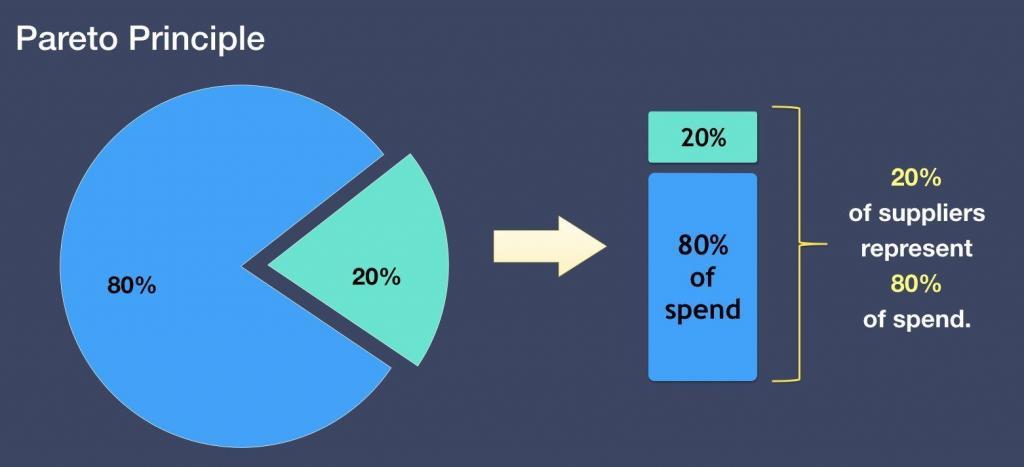

This is a straightforward analysis commonly using the Pareto principle (80/20) that highlights how many suppliers comprise 80% of the spend for each category.

Using this type of analysis we can quickly identify the categories where there are too many suppliers comprising the bulk of the spend.

These categories are then flagged for “further detailed analysis”.

My personal preference is to take the Pareto principle a couple of steps further and conduct a 70/20/10 analysis – showing how many suppliers comprise 70% of the spend and how many suppliers comprise the bottom 20% and the bottom 10% (although the breakout can be anything).

This yields enhanced visibility into the number of suppliers that make up 70% (or 80%) of the spend along with the number in the bottom 20% and the bottom 10% of each category.

The additional 20/10 buckets allow us to see how many small suppliers we are managing for each category – additional consolidation opportunities.

Many organizations have some sort of preferred supplier list either managed in a procurement system or sitting in a spreadsheet on someone’s computer.

Including this information in the spend analysis application will provide immediate visibility into two areas:

- categories where preferred suppliers are in place but not in use

- categories where no preferred supplier exists, thus highlighting a potential sourcing opportunity.

4. Spend by Buying Channel

One of the benefits of spend analysis is that it helps to identify process inefficiencies.

The buying channel, or source system, identifies where each transaction originated.

Companies with procurement systems in place can quickly identify business units/individuals that are circumventing existing processes.

Driving spends towards approved buying channels will improve overall controls, yield better compliance, improve data quality, lead to faster sourcing cycles, provide term discount opportunities and reduce A/P costs associated with check requests.

Sure, many of these or not tangible savings, but substantial benefits nonetheless.

5. Purchase Price Variance

“Are we buying the same items across our locations and paying different prices”? We are finding this to be one of the first areas our customers look – and they generally find some immediate wins.

By including line item level information (with associated parts/items if applicable) will quickly enable you to zero in on these opportunities.

6. Sourcing Compliance

This type of analysis begins to move away from the basic spend analysis towards sourcing execution management.

At this stage we have used the spend analysis application to identify sourcing and/or savings opportunities and sourcing initiatives have been completed – i.e. we have sourced a category and a new contract is in place.

While there are numerous areas associated with compliance, we can start with the basics. Including our contract award information in our spend application will unlock the ability to manage and measure our performance across each initiative and ultimately track savings.

To learn more on How to conduct a better Spend Analysis, download your free e-book here: